Climate, Environment & Emergency Management: News to Know

July 16, 2025

A. Central Texas Flooding

Collier, Dillon, “Director Who Helped Bring CodeRED to Kerr County Says Leadership Lost Sight of Tool’s Value,” KSAT (July 11, 2025).[1]

Gilbert, David and Taft, Holly, “Conspiracy Theories About the Texas Floods Lead to Death Threats,” Wired (July 8, 2025).[2]

On Sunday afternoon, Michael Meyer, the founder of anti-government extremist group Veterans on Patrol, posted a warning on his Telegram channel. “Due to the recent weather weapon deployed against Texas, which resulted in a high number of child murders, efforts to eliminate this military treason are being escalated,” Meyer, who is commonly known as Lewis Arthur, wrote.

Hours later, a man broke into an enclosure containing the NextGen Live Radar system operated by News 9 in Oklahoma City, damaging its power supply and briefly knocking it offline. The man also damaged CCTV cameras monitoring the site, but footage shared by News 9 shows the cameras captured a clear image of his face before they were destroyed.

Meyer, who declined to tell WIRED whether he knew the identity of the perpetrator, says the attack was part of what he calls Operation Lone Wolf, adding that he’s in discussion online with over a dozen people who are willing to carry out similar attacks. “Anyone that's going out to eliminate a Nexrad, if they haven't harmed life, and they're doing it according to the videos that we're providing, they are part of our group,” Meyer tells WIRED. “We're going to have to take out every single media's capabilities of lying to the American people. Mainstream media is the biggest threat right now.”

Nexrads refer to Next Generation Weather Radar systems used by the National Oceanic and Atmospheric Administration to detect precipitation, wind, tornadoes, and thunderstorms. Meyer says that his group wants to disable these as well as satellite systems used by media outlets to broadcast weather updates.

The attack on the News 9 weather radar system comes amid a sustained disinformation campaign on social media platforms including everyone from extremist figures like Meyer to elected GOP lawmakers. What united these disparate figures is that they were all promoting the debunked conspiracy theory that the devastating flooding in Texas last weekend was caused not by a month’s worth of rain falling in the space of just a few hours—the intensity of which, meteorologists say, was difficult to predict ahead of time—but by a targeted attack on American citizens using directed energy weapons or cloud seeding technology to manipulate the weather. The result has not only been possible damage to a radar system but death threats against those who are being wrongly blamed for causing the floods.

…. within hours of the tragedy happening, conspiracy theorists, right-wing influencers, and lawmakers were pushing wild claims on social media that the floods were somehow geoengineered.

“Fake weather. Fake hurricanes. Fake flooding. Fake. Fake. Fake,” Kandiss Taylor, who intends to run as a GOP candidate to represent Georgia’s 1st congressional district in the House of Representatives, wrote in a post viewed 2.4 million times. “That doesn’t even seem natural,” Kylie Jane Kremer, executive director of Women for America First, wrote on X, in a post that has been viewed 9 million times.

…. Cloud seeding—the practice of increasing precipitation in a cloud by introducing materials like silver iodide or dry ice—has been in use for decades. The Texas Department of Licensing and Regulation maintains a page on current weather modification efforts from irrigation districts, counties, and other groups in the state….

Multiple meteorologists told WIRED that there is no way that cloud seeding was responsible for the devastating storms that racked Texas last week. “It is not physically possible or possible within the laws of atmospheric chemistry to cloud seed at a scale that would cause an event like [the Texas flooding] to occur,” says Matt Lanza, a digital meteorologist based in Houston. Lanza compares cloud seeding to adding “icing to a cake”: It’s able to juice up precipitation from clouds in drier areas, not create storms wholesale out of thin air.

Jaffe, Logan, “Oral Histories From Kerr County, Texas, Show a Long Local Knowledge of Floods,” ProPublica Dispatches (July 12, 2025).[3]

As we wait for answers — or as journalists dig for them — the oral histories show Kerr County residents have warned each other, as well as newcomers and out-of-towners, about flooding for a long time. In his 2000 oral history, Secor said he remembered a time in the spring of 1959 when his own father tried to warn one new-to-town woman about building a house so close to the river.

“He took her out and showed her the watermarks on the trees in front of our house and all,” Secor said, likely referring to the watermarks from the flood of 1932, which a local newspaper described at the time as “the most disastrous flood that ever swept the upper Guadalupe Valley.” The flood killed at least seven people.

“‘Oh,’ she says, ‘that will never happen again,’” Secor recalled.

He said her body was found in a tree a few months later after a flood swept her and the roof she stood on away.

Jimenez, Elisabeth, “Hays County Officials Approve Plan to Brace For Floods, Hailstorms, More,” Community Impact (July 14, 2025).[4]

Hays County Commissioners approved the county’s latest multi-jurisdiction plan to mitigate weather hazards as the area continues to grapple with flood risks, severe storms, drought and more. The Commissioners Court unanimously approved the 2025 Multi-Jurisdiction Hazard Mitigation Plan at a meeting July 8.[5]

….. The plan details a list of priority actions for the jurisdictions to incorporate. The priorities are ranked from low to high priority. County and city stakeholders created their priority items to best fit their jurisdiction, meaning not every jurisdiction holds the same priorities. Some high priority items from the various jurisdictions include, but are not limited to:

Structurally reinforcing buildings for natural hazards such as wind, floods, etc. in critical county and city buildings;

Continue purchase of backup emergency generators in critical buildings in Hays County;

Continue efforts to improve and expand existing low-water crossing and road blocking systems;

County will pursue potential options to provide discounts to flood policy holders;

Voluntary buyouts for one or more affected properties in the City of Buda; and

Installation of permanent weather radio system and weather station at Dripping Springs City hall with back-up power source.

High priority actions will be implemented immediately as funding becomes available, according to the mitigation plan document.

…. “While large portions of the County remain rural in nature, the regional population and economic growth is being felt in the area and underscores the need to plan for mitigation of future hazards to protect people and property,” the mitigation plan states. Additionally, a rise in more frequent, violent weather events and its potential impact on communities and their property pushes the need for the new mitigation plan, as stated in the document.

“With climate change affecting weather patterns and sea level rise on the Texas coast, these and other hazards are forecast to become more frequent and greater in magnitude in the future,” the document states.

The mitigation plan listed hazards such as floods, wildfires and extreme heat as highly likely of frequency from 1997-2023, with medium to high severity levels. For example, floods events from 1997-2023 had a high likelihood of frequency, with high severity, property damages over $224.63 million, crop damages costing $330,000, 15 deaths and over 175 injuries. Hailstorms had the second highest cost in property damage at over $100.7 million, despite a lower rate of frequency.

The mitigation plan points to flooding and hailstorms as “priority hazard[s] from which to protect people and property within the Hays County planning area.” Other likely hazards include droughts, hailstorms, severe winterstorms and windstorms as likely, with low to high severity levels.

Judge Ruben Becerra said recent floods in Kerr County and surrounding Central Texas areas demonstrated the importance of alert systems and hazard infrastructure. “We have a system in place that is helping us protect our residents in ways that others don't," he said at the July 8 meeting. “That was made abundantly clear over this weekend.”

…. Following approval of the 2025 mitigation plan, participating jurisdictions will work on their priority list of action items. Stakeholders will work on implementing the action items with timelines ranging from within the next two years to more than five years.

Lonsdorf, Kat, “In the Texas Flood Zone, Volunteers Help Reunite Lost Pets With Their Owners,” NPR (July 12, 2025).[6]

NPR Staff, “Photos: Before-and-After Satellite Images Show Extent of Texas Flooding Destruction,” NPR (July 10, 2025).[7]

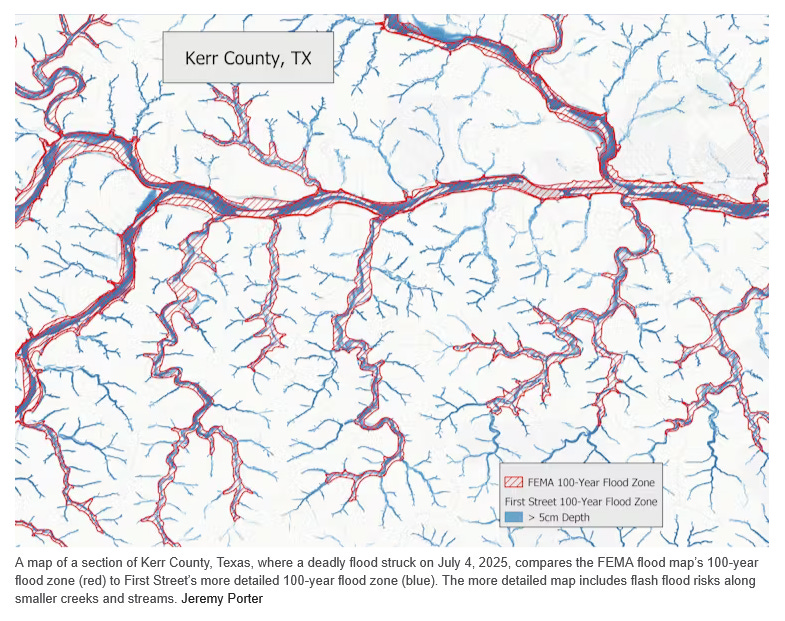

Porter, Jeremy, “FEMA’s Flood Maps Often Miss Dangerous Flash Flood Risks, Leaving Homeowners Unprepared,” The Conversation (July 13, 2025).[8]

Deadly and destructive flash flooding in Texas and several other states in July 2025 is raising questions about the nation’s flood maps and their ability to ensure that communities and homeowners can prepare for rising risks.

The same region of Texas Hill Country where a flash flood on July 4 killed more than 130 people was hit again with downpours a week later, forcing searchers to temporarily pause their efforts to find missing victims. Other states including New Mexico, Oklahoma, Vermont and Iowa also saw flash flood damage in July.

The U.S. Federal Emergency Management Agency’s flood maps are intended to be the nation’s primary tool for identifying flood risks. Originally developed in the 1970s to support the National Flood Insurance Program, these maps, known as Flood Insurance Rate Maps, or FIRMs, are used to determine where flood insurance is required for federally backed mortgages, to inform local building codes and land-use decisions, and to guide flood plain management strategies.

In theory, the maps enable homeowners, businesses and local officials to understand their flood risk and take appropriate steps to prepare and mitigate potential losses. But while FEMA has improved the accuracy and accessibility of the maps over time with better data, digital tools and community input, the maps still don’t capture everything – including the changing climate. There are areas of the country that flood, some regularly, that don’t show up on the maps as at risk.

I study flood-risk mapping as a university-based researcher and at First Street, an organization created to quantify and communicate climate risk. In a 2023 assessment using newly modeled flood zones with climate-adjusted precipitation records, we found that more than twice as many properties across the country were at risk of a 100-year flood than the FEMA maps identified.

Even in places where the FEMA maps identified a flood risk, we found that the federal mapping process, its overreliance on historical data, and political influence over the updating of maps can lead to maps that don’t fully represent an area’s risk.

What FEMA Flood Maps Miss

FEMA’s maps are essential tools for identifying flood risks, but they have significant gaps that limit their effectiveness. One major limitation is that they don’t consider flooding driven by intense bursts of rain. The maps primarily focus on river channels and coastal flooding, largely excluding the risk of flash flooding, particularly along smaller waterways such as streams, creeks and tributaries.

This limitation has become more important in recent years due to climate change. Rising global temperatures can result in more frequent extreme downpours, leaving more areas vulnerable to flooding, yet unmapped by FEMA.

For example, when flooding from Hurricane Helene hit unmapped areas around Asheville, North Carolina, in 2024, it caused a huge amount of uninsured damage to properties.

Even in areas that are mapped, like the Camp Mystic site in Kerr County, Texas, that was hit by a deadly flash flood on July 4, 2025, the maps may underestimate their risk because of a reliance on historic data and outdated risk assessments.

Additionally, FEMA’s mapping process is often shaped by political pressures. Local governments and developers sometimes fight to avoid high-risk designations to avoid insurance mandates or restrictions on development, leading to maps that may understate actual risks and leave residents unaware of their true exposure.

An example is New York City’s appeal of a 2015 FEMA Flood Insurance Rate Maps update. The delay in resolving the city’s concerns has left it with maps that are roughly 20 years old, and the current mapping project is tied up in legal red tape.

On average, it takes five to seven years to develop and implement a new FEMA Flood Insurance Rate Map. As a result, many maps across the U.S. are significantly out of date, often failing to reflect current land use, urban development or evolving flood risks from extreme weather.

This delay directly affects building codes and infrastructure planning, as local governments rely on these maps to guide construction standards, development approvals and flood mitigation projects. Ultimately, outdated maps can lead to underestimating flood risks and allowing vulnerable structures to be built in areas that face growing flood threats.

New advances in satellite imaging, rainfall modeling and high-resolution lidar, which is similar to radar but uses light, make it possible to create faster, more accurate flood maps that capture risks from extreme rainfall and flash flooding.

However, fully integrating these tools requires significant federal investment. Congress controls FEMA’s mapping budget and sets the legal framework for how maps are created. For years, updating the flood maps has been an unpopular topic among many publicly elected officials, because new flood designations can trigger stricter building codes, higher insurance costs and development restrictions.

In recent years, the rise of climate risk analytics models and private flood risk data have allowed the real estate, finance and insurance industries to rely less on FEMA’s maps. These new models incorporate forward-looking climate data, including projections of extreme rainfall, sea-level rise and changing storm patterns – factors FEMA’s maps generally exclude.

Real estate portals like Zillow, Redfin, Realtor.com and Homes.com now provide property-level flood risk scores that consider both historical flooding and future climate projections. The models they use identify risks for many properties that FEMA maps don’t, highlighting hidden vulnerabilities in communities across the United States.

Stephens, Keri and Bean, Hamilton, “Why It Can Be Hard to Warn People About Dangers Like Floods – Communication Researchers Explain the Role of Human Behavior,” The Conversation (July 11, 2025).[9]

Research shows that effective warning messages need to include five critical components:

A clear hazard description,

Location-specific information,

Actionable guidance,

Timing cues and

A credible source.

The Federal Emergency Management Agency’s integrated public alert and warning system message design dashboard assists authorities in rapidly drafting effective messages.

This warning system, known as IPAWS, provides nationwide infrastructure for wireless emergency alerts and Emergency Alert System messages.[10] While powerful, IPAWS has limitations − not all emergency managers are trained to use it, and messages may extend beyond intended geographic areas. Also, many older mobile devices lack the latest capabilities, so they may not receive the most complete messages when they are sent.

Hyperlocal community opt-in systems can complement IPAWS by allowing residents to register for targeted notifications. These systems, which can be run by communities or local agencies, face their own challenges. People must know they exist, be willing to share phone numbers, and remember to update their information. Social media platforms add another communication channel, with emergency managers increasingly using social media to share updates, though these primarily reach only certain demographics, and not everyone checks social media regularly.

The key is redundancy through multiple communication channels. Research has found that multiple warnings are needed for people to develop a sense of urgency, and the most effective strategy is simple: Tell another person what’s going on. Interpersonal networks help ensure the message is delivered and can prompt actions. As former Natural Hazards Center Director Dennis Mileti observed: The wireless emergency alerts system “is fast. Mama is faster.”

Professionals from the National Weather Service, FEMA and the Federal Communications Commission, along with researchers, are increasingly concerned about warning fatigue – when people tune out warnings because they receive too many of them. However, there is limited empirical data about how and when people experience warning fatigue – or about its impact.

This creates a double bind: Officials have an obligation to warn people at risk, yet frequent warnings can desensitize recipients. More research is needed to determine the behavioral implications of and differences between warnings that people perceive as irrelevant to their immediate geographic area versus those that genuinely don’t apply to them. This distinction becomes especially critical when people might drive into flooded areas outside their immediate vicinity.

B. Other News

Cooper, Ryan, “Climate Change Will Bankrupt the Country,” The American Prospect (June 20, 2025).[11]

Cosier, Susan, “As Data Centers Proliferate Across Illinois, Communities Grapple with How to Supply the Necessary Water,” Inside Climate News (June 16, 2025).[12]

Once they’re online, data centers require a lot of electricity, which is helping drive rates up around the country and grabbing headlines. What gets less attention is how much water they need, both to generate that electricity and dissipate the heat from the servers powering cloud computing, storage and artificial intelligence.

A high-volume “hyperscale” data center uses the same amount of water in a year as 12,000 to 60,000 people, said Helena Volzer, a senior source water policy manager for the environmental nonprofit Alliance for the Great Lakes.

Increasingly, residents, legislators and freshwater advocacy groups are calling for municipalities to more carefully consider where the water that supplies these data centers will come from and how it will be managed. Even in the water-rich Great Lakes region, those are important questions as erratic weather patterns fueled by climate change affect water resources.

When it comes to siting data centers, “we don’t see a lot of coordination or long-term thinking about water,” said Michelle Stockness, executive director of Freshwater Society, a nonprofit focused on water preservation.[13] Some places cannot support data centers, she said, “and you’ll have water-use conflicts if you put them there.”

Illinois already has more than 220 data centers, and a growing number of communities interested in the attendant tax revenue are trying to entice companies to build even more. Many states in the Great Lakes region—Illinois, Indiana, Michigan and Minnesota among them—are offering tax credits and incentives for data center developments. The Illinois Department of Commerce and Economic Opportunity has approved tax breaks for more than 20 data centers since 2020.

…. Much of the water used in data centers never gets back into the watershed, particularly if the data center uses a method called evaporative cooling. Even if that water does go back into the ecosystem, deep bedrock aquifers, like the Mahomet in central Illinois, can take centuries to recharge. In the Great Lakes, just 1 percent of the water is renewed each year from rain, runoff and groundwater.

…. Non-disclosure agreements that companies ask municipalities to sign when they propose a data center further obscure how much water is needed and where it would come from, making it difficult to determine whether municipalities have enough supply, said Volzer, with Alliance for the Great Lakes.[14]

To help combat that, some states in the region like Ohio and Indiana are now conducting regional water-demand studies, which would help communities determine where water is available before approving a data center. Some water managers are also conducting those studies in Illinois, but they are not required.

Green, Amy and Aldhous, Peter, “Florida’s Home Insurance Crisis Hits Hardest in Some of the State’s Poorest Counties,” Inside Climate News (July 6, 2025).[15]

Insurance experts have warned repeatedly that rising economic losses from extreme weather events driven by climate change threaten the industry with collapse—and with it, housing markets and families’ finances. Together with Louisiana and wildfire-wracked California, Florida, threatened by tropical cyclones barreling into its coasts, is where the crisis is hitting hardest.

The risk is driving insurance companies to raise rates and withdraw from markets entirely, a situation that itself represents a crisis threatening to destabilize what for many Americans is their most important asset, their home.

Much attention has focused on the threats to pricey real estate and resulting high premiums along the coast of South Florida. But an Inside Climate News analysis of data on home insurance non-renewals shows that already disadvantaged inland rural communities around Lake Okeechobee are an overlooked epicenter of the state’s insurance crisis.

That finding stems from data released in December by the U.S. Senate Committee on the Budget. The Senate committee asked large insurance companies to disclose the number of policies that were not renewed each year from 2018 to 2023.[16] Committee staffers received data from 23 companies, collectively accounting for about two-thirds of the home insurance market across the nation. (The committee said it focused on non-renewals because industry experts say high non-renewal rates represent an early warning sign of market destabilization.)

The committee’s report drew a direct connection to climate change, noting that spiking non-renewal rates in 2022 and 2023 were concentrated in the counties facing the highest risk of climate-related disasters.[17] “The stuff that scientists have predicted for decades about climate change is now starting to come true, and the leading indicator of that is the insurance industry,” Senator Sheldon Whitehouse (D-R.I.), chairman of the committee at the time of the report’s release, told Inside Climate News.

Insurance companies “look at places like Florida—which is seeing a combination of sea level rise and worsened storm activity and warming oceans around the state on three sides of it and more moisture held in the warmer air above it so that rain bursts are more dangerous—and they are starting to realize, ‘Wow. That’s going to be more risk than we can bear, and it’s also really hard to predict,’” he said. “So that makes Florida—as they used to say in the movies—the preview of coming attractions.”

…. non-renewals were highest in the Florida counties where climate-related hazards are compounded by poverty and other factors that make it harder to withstand and recover from extreme weather events. Glades County, with a median household income of less than $39,000 a year compared to the statewide figure of around $72,000, had the highest non-renewal rates and is the state’s poorest county.

…. “What we’re seeing here is a recognition of the risk of these storms causing damage anywhere in the state. I don’t think there is any part of Florida that is safe from storms,” said Chuck Nyce, a professor of risk management and insurance at Florida State University.[18] “I think you’re seeing that companies really made a conscious effort to reduce their risk from central Florida, south.”

Meanwhile, a growing scarcity of insurance is but one aspect of the crisis facing Florida, especially the underserved counties of the state’s heartland. Policies also are increasingly unaffordable. The situation means that the homeowners who are most at risk of losing insurance are those with the least resources for dealing with disasters, and with no insurance they are even more exposed.

…. Doc Thrift, 69, initially put his Okeechobee house up for sale after receiving a renewal notice for $14,500. Thrift, who is experienced in construction, has lived for the last 20 years in a 2,000-square-foot stucco home his late wife designed and he built almost entirely himself. His wife suffered from a neuromuscular disease and died five years ago. He now lives here alone with his dog, Jake. He eventually decided he could not part with the home and took out a personal loan to pay off the mortgage so that he can go without insurance, as many people he knows are doing.

…. Problems obtaining insurance from large, established providers will drive homeowners into the arms of companies vulnerable to insolvency. In her research into the Florida insurance market, Senator has tracked the withdrawal of major insurance providers from the state and their replacement by smaller firms that have proved vulnerable to insolvency.

“Insurers are leaving, and they are in no means wanting to come back,” Sen said. “The ones that are replacing them are of low quality.” …. Seven Florida insurers became insolvent in the 13 months between January 2022 and February 2023.

Gross, Liza, “US Labor Advocates Demand Heat Protections for Workers as Planet Warms,” Inside Climate News (June 17, 2025).[19]

…. In the absence of federal action to protect workers from extreme heat, seven states have passed their own standards, though most have exemptions that leave workers at risk. Two workers died last year in states with some sort of heat rule.

…. Colorado’s heat rule applies only to agricultural workers. And in 2024, the hottest year on record, Florida Governor Ron DeSantis signed a law prohibiting municipalities from implementing their own heat rules, following Texas, which passed a ban the year before.

Honore, Marcel, “Hawaii Makes History As First State To Charge Tourists To Save Environment,” Honolulu Civil Beat (May 27, 2025).[20]

Hawaii has officially become the first U.S. state to enact a so-called “green fee” — a charge added onto hotel room stays and other short-term visits to help protect the local environment and address the growing impacts of climate change.

…. Specifically, the revenue will come from a .75% increase on the tax Hawaii visitors pay on their nightly hotel and short-term stays. The uptick raises the state’s transient accommodations tax, or TAT, to 11%. Visitors already pay an additional 3% TAT on their stays to the counties. That will translate to visitors paying about $3 extra, Green said, on a $400 room stay.

Irfan, Umair, “It’s Not Just the Cities. Extreme Heat is a Growing Threat to Rural America,” Vox (June 24, 2025).[21]

Now researchers have found that rural areas may suffer more under extreme heat than previously thought. A report from Headwaters Economics and the Federation of American Scientists found that more than half of rural zip codes in the United States, which includes some 11.5 million Americans, have “high” heat vulnerability, a consequence not just of temperatures but unique risk factors that occur far outside of major cities.[22]

…. A major factor: the median age of the rural population is older than in cities. That matters, because on a physiological level, older adults struggle more to cope with heat than the young. People living in rural communities also have double the rates of chronic health conditions that enhance the damage from heat like high blood pressure and emphysema compared to people living in urban zip codes.

Rural infrastructure is another vulnerability. While there may be more forests and farms in the country that can cool the air, the buildings there are often older, with less adequate insulation and cooling systems for this new era of severe heat. Manufactured and mobile homes, more common in rural areas, are particularly sensitive to heat. In Arizona’s Maricopa County, home to Phoenix, mobile homes make up 5 percent of the housing stock but account for 30 percent of indoor heat deaths.

Even if rural residents have air conditioners and fans, they tend to have lower incomes and thus devote a higher share of their spending for electricity, up to 40 percent more than city dwellers, which makes it less affordable for them to stay cool. That’s if they can get electricity at all: Rural areas are more vulnerable to outages due to older infrastructure and the long distances that power lines have to be routed, creating greater chances of problems like tree branches falling on lines. According to the US Census Bureau, 35.4 percent of households in rural areas experienced an outage over the course of a year, compared to 22.8 percent of households in urban areas.

Sparsely populated communities also have fewer public spaces, such as shopping malls and libraries, where people can pass a hot summer day. Rural economies also depend more on outdoor labor, and there are still no federal workplace heat regulations. Farmworkers, construction crews, and delivery drivers are especially vulnerable to hot weather, and an average of 40 workers die each year from extreme heat.

The health infrastructure is lacking as well. “There is a longstanding healthcare crisis in rural areas,” said Grace Wickerson, senior manager for climate and health at the Federation of American Scientists.[23] There aren’t always nearby clinics and hospitals that can quickly treat heat emergencies. “To really take care of someone when they’re actually in full-on heat stroke, they need to be cooled down in a matter of minutes,” Wickerson said.

Myers, Katie, “Seeing Fewer Fireflies This Year? Here’s Why, and How You Can Help,” Grist (July 11, 2025).[24]

Author’s Note: Hays County, where I live, is approximately 100 miles from Kerr County, the epicenter of the July 4th floods. That’s why emergency planning information for it is relevant.

As usual, see the attached PDF for additional graphics and the full text of this edition.

Does anyone know if the belief that Democrats are geo-engineering the weather has a significant following with important people or if it is mostly just a belief of the ultra fringe.

I'm having trouble believing that there is any significant group that believes Democrats can control the weather.

The Delusional Maga Idiotic Cult believes in the stupid Qanon cult led by the same cult idiots who started the stupid conspiracy theories and the maga cult are dumb enough to believe what MTG is conspiring to spread lies and misinformation! No one can control the weather!!